I started this blog amid the coronavirus because i am interested in finance and investing or you can say that i don’t have any other productive thing to do so but at first i didn’t think of starting a blog but I want to gain more knowledge on investment and personal finance for myself I starts researching on a topic then made my on notes to get a clear understanding of them but soon i thought it would be better if i share my notes through blogging then it might be good. So from there my journey to writing were started and I created this blog-THEMILLENNIALINVESTOR and initially I started writing on investment topics, and personal finance. I also got a good response for some of my blogs, then I get an idea that i could become a financial writer as i am loving what i am doing So i thought lets do this professionally by making a purchasing a good domain name and hosting but then i realise that i don’t have the most important thing that i need to start writing on my first professional blog i.e., Talent(nahhhh) then Money(Yesssssss), i don’t have enough money to buy a decent hosting and domain that time so there are two option for me the first one is to ask for some money from family(that i don’t want to do ) and secondly, I should do some part time work online(now that’s the option I chose). At that time, i though that what type of work i can do that gives me some decent money for my work amid the coronavirus crisis, then i thought that i like to writing so lets find some work in content writing field after applying to some internships. finally, i get an offer letter from a decent company for writing about cars(and cars is my second love) that also pays me not great but i accept it because i myself is not believing that, how can someone pay me money for writing(at that time maybe i am not a good writer like chetan bhagat) but i was happy, So i did that internship for 6 months though i thought i would do this only for 2 months to get some money and starts my blog but you know that was the first time i am earning and you know money is something that gives you some independence, as between these 6 months i didn’t ask for a single penny from my family, and you know that feeling where you can buy anything you want without asking from parents, is one of the best feeling i have ever had because that gives me a sense of responsibility and enjoyment. That was my first financial freedom moment to me. but all these 6 months aren’t good for me development wise(as at some point, i was kind of bore of writing the same thing again and again(just about cars) though i like cars but i like other things too and from that moment i decided to leave it and work on my own blog but it is easy to say that i will leave but we know all the reward that attach with the job will also leave with the job but i have to take this decision cause if i just struck in that job, my growth will be stop mentally and i am not able to work on what i love.

Now, many people will think we can do two thing simultaneously like before the internship I thought I can do work on both blogging and internship but you know really its very difficult and it almost depends on the environment you are because my environment is not much good so i can’t concentrate on both things and I have to choose one so at that time, I chose the latter one.

As the time of writing this i decided to start the blogging again and I hope this time I would choose this before anything.

Millennial is the generation which are smarter than their parents, or Gen X, millennial have more access to technology, more excess to knowledge, and most importantly they have more excess to freedom as compared to their parents, millennial can spend their money on whatever they want, in the persuasion of their what they want like spends on fashion, car, luxurious things, and due to following ongoing trends they usually make money mistakes in their early age

we may not forget our parents”s perception towards money, their spending and saving habits, they were more into saving rather than spending on unnecessary things.I know millennial is the age when we are more carefree and want to explore the world which is somewhere good thing but we just need to keep something in my mind before spending money without any thought, i have 5 points to share with you that show the money mistakes usually millennial make

Don’t make a budget

Not creating an emergency fund

Following the mindset of earn more spend more

Not invest in knowledge

not saving for retirement

Rely on credit

I have found that many millennial don’t make a budget which is really very important, because budget enables us how to live with the given money, For e.g A and b both has $2000 salary p.m. A always make a budget before spending their money, on the other hand B is a fun loving person he don’t make a budget before spending money. Now, what happens we may know, that at the end of the day B is in problem because he end up paying bills for the unnecessary things that are not essential to live and he also didn’t save money for the rainy day

Books are a good way to increase knowledge and know about something. Investing is one of the thing that is very important and many people want to know more about it. So, we have compiled 5 investing books for beginner that surely helps them to know ups and down of investing

The Intelligent Investor

The Intelligent Investor is by far the best book on Investing” said by Warren Buffet, the most successful investor of modern world. The Intelligent Investor provides the framework that must be needed to excel in investing. The Intelligent Investor teaches time-tested principles that every investor can use.

Common Stocks and uncommon Profit

Philip Fisher has had a major influence on modern investment theory and is credited with the idea of analyzing stocks based on their growth potential. Common Stocks and Uncommon Profits teaches investors to analyze the quality of a business and its ability to produce profits. First published in the 1950s, Fisher’s lessons are just as applicable today, more than a half-century later.

Another Investment Classic book is Common Stocks and uncommon Profit by Philip Fisher. This books emphasis on choosing the stocks based on their growth potential. Common Stocks and Uncommon Profits teaches investors to analyze the quality of a business and its ability to produce profits. First published in the 1950s, Fisher’s lessons are just as applicable today, more than a half-century later.

Learn to Earn

Learn to Earn written by Peter Lynch is one of his three books, other books are One Up on Wall Street (1989), or Beating the Street (1993). Peter Lynch who is widely known for as a manager of the spectacularly-performing Fidelity Magellan Fund. Under his Leadership, the fun has increased from $18 million to whopping $14 billion Assets under management (AUM). During this time, the fund boasted average returns of more than 29.2% per year. Learn to Earn explains many business basics, while One Up on Wall Street makes the case for the benefits of self-directed investing.

Rich Dad Poor Dad

Rich Dad Poor Dad is one of the best books on Personal Finance. In which Kiyosaki’s view is that the poor and middle class work for money, but the rich work to learn. He stresses the importance of financial literacy and presents financial independence as the ultimate goal to avoid the rat race of corporate America.

The author points out that while accounting is important to learn, it can also be misleading. Banks label a house as an asset for the individual, but because of the required payments to keep it, it can be a liability in terms of cash flow. Real assets add cash flow to your wallet. Kiyosaki also highlights the importance of tax planning.

Think and Grow Rich

Think and Grow Rich” was written during the Great Depression, and has since sold more than 100 million copies worldwide. Hill conducted extensive research based on his associations with wealthy individuals during his lifetime. At the suggestion of Andrew Carnegie, Hill published 13 principles for success and personal achievement from his observations and research. This book conveys valuable insights into the psychology of success and abundance and should be considered a priority read given the current period’s emphasis on shock-value entertainment and negative news.

Millennials carry much of this burden and have one of the highest student loan balances of any generation. The average student loan balance among millennials—consumers between the ages of 23 and 38—was $34,504 in the first quarter (Q1) of 2019, an 8% increase from Q1 of 2018.Every year students are graduating from colleges to get their dream job but you know Two-Third of students takes education loan to complete their education, Education cost is rising at the rate of 15% P.A.These education loan can be a burden in the beginning of their careers. With the average salary of about $50,000 in which they need to pay a Monthly instalment and manage their personal expenses too including the emi of car,hoam etc, its a quite discussion over this topic that is your student loan worth because if you compared the opportunity costs of an average student loan maybe you can do other productive things like starting your own business and giving jobs to others rather than be an employee of someone else etc.So i am gonna share with you some facts and views regarding this

Choose your degree wisely-Not all majors have same income potential

For a teenage student it would be difficult and confusing to pick your major wisely, specially for those who doesn’t have any mentor or those who are first generation learner.Some students pick their careers according to their interest and some of them choose to attend their dream college,which further result in changing the course almost 30% students change their majors during their college time.

Students who majors in STEM earns the highest salary as compared to others majors,which is followed business then economics etc.Student loan are very important and big decision for student because he has to bear it for many years after completing their college.So, do some own research and take guidance from some experienced person before picking up a course.

College graduated may have more financial stability

College graduates have more financial stability as compared to those who doesn’t have.Investment in education is a good option.The pay gap between a college graduate and high school diploma is very high.The earnings of people would continue to rise with the rise of education level.The level of unemployment will also high for no-graduates.People having college degree have a healthy lifestyle and better financial stability.

Different colleges have different costs

The college cost of colleges are different mainly private college demand more fees as compared to public university, There are many students who take admission in college because of various reasons like for having a tag of that college,maybe the college is near to their house,maybe the college have big campus etc these perception and decision of students towards college make them to choose college without concern over its cost which is an important factor.So, it is better to choose your college as per your affordability and your subject interest.

Bottom Line

While college graduates can earn a good income yet it doesn’t mean that education loan worth it.While taking an education loan it better to consider the various factor that comes with it because it will cost you and your family’s finances for a decade its better to go for scholarship and financial aid first then look for student loan and if you borrow then its your responsibility to make most out of your college time, do better at college,make networking and be competent.

That’s all. I hope this post on ‘Education loan and Millennial’ is useful to the readers. Further, If you find this post helpful and want me to write more contents on any similar topic, please comment below.

During this coronavirus pandemic search for work from home, jobs have surged, we know that this coronavirus has led to millions of layoffs by companies, almost 10 million people in the US has filed for unemployment and this situation creates many problems for people and now people are moving towards this remote jobs but some people have a perception that we can’t earn that much money through which we can sustain our lives and to break this stereotype I am gonna share with some of the highest-paying remote jobs which you can do at the comfort of your home.

Web developer

Web developer creates and manages websites for companies. This is also a growing career as every company needs websites today and for creating a website they contact freelance web developers. Web developers typically make around $50,000-$150,000 a year

Bloggers or writers

Blogger is not a new profession now though it takes time to generate regular income from this profession, bloggers or writers write article and blogs for their own websites or for other company’s websites, These bloggers don’t need to go office regularly for their work they can write blogs from anywhere which makes this profession better from others, To be a blogger one must possess deep knowledge related to their field and some skills like content writing, content marketing, etc. A blogger can make around $30,000-$500,000 a year according to their skills and experience.

Virtual assistant

Virtual assistants do all the work of an assistant but at the comfort of their home, they organize meetings, set work schedules, preparing reports, and managing the paperwork. In this profession, you can easily make around $35,000-$90,000 a year

Cloud Designer

Cloud designer also known as cloud architects creates and designs cloud apps and manage the cloud computing related strategies. Those who don’t know what are cloud apps and what they do let me explain to you cloud apps are those apps who stores data on internet servers. Being a cloud architect they need a vast knowledge of the operating system, programming language, and cloud security. They typically make between $70,000-$170,000 a year.

Research engineers

Research engineers make new products on the basis of information and data or make research-backed products for various industries. They make these research-backed products for various industries like software, electrical, mechanical, and aerospace. For being a research engineer one needs to have an engineering degree. Research engineers typically make between $50,000-$125,000 a year

Cyber-security analyst

Cyber-security security analysts guard or protect a company’s computer system and networks for malware and viruses.The research for IT trends, security breaches and creates solutions to stop the hacker from stealing the data from computers.To become a cyber-security expert you need to have degree with some IT experience.Cyber-security analysts typically make $50,000-$125,000 a year

Mobile developers

Mobile developers or App developers create apps for android phones and ios. With the increase of smartphones this profession also grown, to be an app developer you muse possesses the required knowledge and skills like coding skills and proficiency in a programming language. Mobile developers can make $50,000-$120,000 a year.

PR directors

PR directors are mainly work in improving and managing the company’s public image. They basically work in teams to enhance the public’s perception of a company by writing press releases, organizing corporate events, etc. To be a PR director one must possess vast experience of at least 10 years. They typically make around between $55,000-$130,000 a year.

Psychologists and Therapist

Psychologists and therapist use various therapy to solves people mental health issues and addiction, to be a psychologist one needs to have an advanced degree in psychology and some experience. They typically make around $45,000-$120,000 a year

Front-end developers

Front-end developers work on designs and visuals of a website and Apps. One needs to have an excellent command over programming language like ruby, java, SQL to produce the commands that make visuals of a website or app. They need some back-end job experience and they can make around $45,000-$120,000 a year

So these are some of the highest paying work from home job but one need to possess the required knowledge and skill of a specific profession, That’s all. I hope this post on ‘10 Highest-paying Work from home jobs’ is useful to the readers. Further, If you find this post helpful and want me to write more contents on any similar topic, please comment below.

As the technology grows rapidly more and more Businesses are being started and finance is the blood of any business to grow business financing is very important, nowadays entrepreneurs have a growing number of options to consider and determining and selecting the lender is bit difficult because of some of its advantages and disadvantages.

But there are two lending options which continuously considers as “best bank loans” are bank loans for business and SBA loans. As they are the lowest cost options available, and also offer the better flexible repayment terms, but sometimes also become hard for some businesses to qualify for getting a loan

Let’s compare SBA vs. business loans based on some common factors and which is right for your specific business needs

The basic difference between a SBA loan and Business loan is SBA loan is partially guaranteed by the government.

SBA LOANS

Requirements

To qualify for SBA loan, one must operate a small but a profitable business which engaged or having territories in the U.S and the owner also needs to have a decent equity invested in the business and also having other alternatives financial resources including personal assets before applying for loan.

Collateral

For getting a SBA loan of under $350,000, you don’t need to require personal collateral to secure the loan. It means you can secure a SBA loan without risking your personal assets but regardless of all collateral requirements, all owners with 20% or more stake in the business or any key management person must provide personal guarantees.

Credit score

SBA loans also require good credit score, those applicants with bad credit score could be rejected or fail to get loan, which includes business credit cards or micro-loans these can help small business build business credit score

Specifically, SBA lenders check FICO SBSS score for loans of $350,000 or less in the 7(a) program. You must have a score of not less than 140(out of 300) to pass the SBA pre-screen, but consider credit score of 160 to be safe.

Cash flow

Cash flow is one of the key parameter that any SBA lender will review. Like with traditional bank loans, having solid cash flow numbers is crucial while applying for an SBA loan. Business loan, SBA loan also demands a solid cash flow, if your cash flow is not good or not steady then you should look for some other options.

Business Loan

Collateral

Collateral refers to the tangible assets that are owned by the business owner. Collateral can be equipment, inventory, invoices and real estate etc. If you fail to pay the loan, the bank can seize and sell this asset in order to get their money back. We can also say, the collateral acts as a security and giving relief to the bank’s concern of losing money.

Credit Score

For getting a business loan the better your credit score, the more likely you’ll get a low rate on a loan. In most cases, you’ll need a credit score of at least 600 to acquire a business loan.

Cash flow

Cash flow is an important factor to any successful business. Cash flow can either make or break your business. A steady stream of cash shows lenders that you’re capable of sustaining the loan payments. It’s a representation of your business’ health.

Conclusion

Both SBA loans and conventional loan are lowest cost financing options available to businesses but applying for both loan is a lengthy process and also these aren’t easiest financing options that can be approved but if you are considering it you need to be ready with documents and business related Information to make the application process as smooth as possible and also be prepared to wait.

The intrinsic value of a stock can be found out by means of fundamental analysis. An investor can understand if the stock is undervalued or overvalued. Fundamental analysis looks at various factors of the stock such as PE ratio, EPS, Dividend Yield, etc.

Stock investing requires careful analysis of financial data to find out the company’s true worth. This is generally done by examining the company’s profit and loss account, balance sheet and cash flow statement. This can be time-consuming and cumbersome.

In order to start investing in stock market the first thing you need to do is fundamental analysis of stocks before buying it,and yes fundamental analysis is the most important and crucial factor in stock investing through fundamental analysis you get to know about the company in more detail,about its performance in last 5-10 years, its long term objectives and financial position of the company and many more things which are very important to know because it will directly affect the share price of the stock

So the question here arises is how to do fundamental analysis as a i said there are many things to know the company which is the part of fundamental analysis it become a tedious and time taking task to do this, there are so much things to analyse about the company which sometimes makes investors lethargic and led them to follow other investor and buying what the hot stock in the market which is totally wrong thing you can’t depend on others in stock investing because the share price keeps changing due to volatility and make your wealth comes to nil, and i also know that yes it is a time taking task but still i try to reduce the time and share the key points in details which need our attention more,So i am gonna share with you only those key points which are the most relevant and only need special attention and i believe that this post will give you some useful insights.

FACT : There are over 5,500 stocks listed in the Indian stock exchange. If you start reading the financials (balance sheet, profit-loss statement, etc.) of all these companies, then it might take years.

Gather information about company

The first thing for doing fundamental analysis is you need to gather information about the company,there are many sources from where you can get information about the company. For this purpose, you should read the company’s annual reports, balance sheet, profit & loss account, any news related to the company in particular or the sector, etc. .

RHP(Red Herring Prospectus) : It is a document about the company’s important information like objective or goals of a company,company background,Industry overview etc. You can get this document on SEBI website.

AGM(Annual General Meeting) : This is a meeting in which the ceo of the company shares useful insights related to the company to all the investor, In this meeting the ceo also shares the current performance of the company and what their future plans. You can get this report on the company website and other equity research related website.

Business News : you can keep updated yourself by watching business to know what are the major things happening across the business sectors and also the economic condition of the country.Economic condition can directly effect the stock market so its better to keep updated with the economic condition of the country.

There are also many finance apps and website available which are dedicated to stock investing which also published financial data of the company like moneycontrol which shows financial information like financial ratios and quarterly reports of the company listed in NSE or BSE. You can also refer to comapany’official website there the company published qurterly reports or other financial reports.

Financials analysis of the company

This is the most important step in fundamental analysis and also complex task because you need some finance knowledge in order to do financial analysis of a company.

In order to take better investing decision you need to analyse the financials of the company and for that you need to analyse the financial statement and balance sheet of the company

If you are from commerce or business background than you can easily do financial analysis of a company but if you are non-commerce background there is no need to worry you can still analyse it but first you must need to read about accounting,finance topics you can get easily stuff about this on Youtube or you can read some books then after getting some knowledge about financials of the company you can start doing financial analysis on your own.

For doing financial analysis you need some financial data of the company, then Analyse the past 5-10 year financial data like profit&loss a/c and balance sheet of the company in order to understand better how much growth have the firm done in these past years and these past year data help you understand to anticipate how the firm will grow in future.

The best website to check the financial statements of a company that most people use is SCREENER.in

Ratio Analysis

For the initial screening of the stocks, you can use various financial ratios like PE ratio, P/B ratio, ROE, CAGR, Current ratio, Dividend yield etc

Earnings per share (EPS): EPS tells us how much of a company’s profit is assigned to each share of stock. EPS is calculated as net income (after dividends on preferred stock) divided by the number of outstanding shares.

Price-to-earnings ratio (P/E): This ratio compares the current sales price of a company’s stock to its per-share earnings.

Projected earnings growth (PEG): PEG anticipates the one-year earnings growth rate of the stock.

Price-to-sales ratio (P/S): The price-to-sales ratio values a company’s stock price as compared to its revenues..

Price-to-book ratio (P/B): This ratio, also known as the price-to-equity ratio, compares a stock’s book value to its market value. You can arrive at it by dividing the stock’s most recent closing price by last quarter’s book value per share. Book value is the value of an asset, as it appears in the company’s books. It’s equal to the cost of each asset less cumulative depreciation.

Dividend payout ratio: This compares dividends paid out to the stockholders to the company’s total net income. It accounts for retained earnings—income that is not paid out, but rather, retained for potential growth.

Dividend yield: This, too, is a ratio—yearly dividends compared to share price. It’s expressed as a percentage. Divide dividend payments per share in one year by the value of a share.

Return on equity: Divide the company’s net income by shareholders’ equity to find its return on equity. You might also hear this expressed as the company’s return on net worth.

Understanding the business or company

Before investing money in shares of a company one must need to understand the company first such as in which sector company operate,who are the target audience of the company their business model,its market share,its competitors,its USP(unique selling preposition) its future plans etc.

You should know about the company’s background and management and the factors that would cause a great impact on the company

All this information help the investor to better understand the business and its viability

If you ever follow warren buffet then you must have heard this

“Never invest in a stock. Invest in a business instead. And invest in a business you understand. In other words, before investing in a company, you should know what business the company is in.”

Check the debt

Their are two types of firms one is levered firm and another one is unlevered firm.Levered firm are those firm who uses debt in their capital structure and unlevered firm are those who don’t use debt in their capital structure

So,before investing one need to make sure if the company is a levered firm or unlevered firm because it directly effects your return

If you invests your money in levered firm than might be you get lower return because of the compulsion of paying interest on debt first and then pay dividend if money left out and in unlevered their is no debt, their is chances of getting better return.

But it doesn’t mean you only invest in unlevered firm, you should invest in a firm whose capital structure is optimal having both debt and equity in better proportion,As debt also increases EPS(earning per share)of the investor but take that in mind also A company with huge debt should be avoided.

Analyse future prospect

If you want to invest for long-term, analysing future prospects of a company becomes mandatory.

For analysing future prospects of a company you first need to know about the future goals of a company like their plan for expansion,diversification,mergers & acquisition because these decisions directly affects the share price of the company

We know Share market is very volatile and you can’t predict the value of any share and you also can’t regularly check the changes in your portfolio but if you just know the future prospects or goals of a company than you are able to anticipate the growth of firm.

It is every investor’s responsibility to evaluate a company on the basis of technical and fundamental analysis before deciding on the stock.

Hope you got an idea on how to analyse a stock before investing your hard earned money in it by reading this article That’s all. I hope this post on ‘How to do fundamental analysis on stocks in 10 minutes’ is useful to the readers. Further, If you find this post helpful and want me to write more contents on any similar topic, please comment below.

So i am happy that my last 2 blogs was much appreciated by readers and i get a good response from them so i decided to write more about mutual funds and make it understand them in an easy way.After knowing much about mutual funds i know now you can invest in mutual funds without any doubt but there are still some common things or terms that you need to know before investing,Let’s know some common terms that you must know terms before investing in mutual funds :

NAV

Nav(Net Asset Value) is the sum total of investment value minus expenses divided by the number of units available. Nav shows the performance of mutual funds,Whenever there is any increase in profit NAV will also increase without any change in allocated units and Vice-versa.

Rating

Rating is the score given to financial product after analysing and evaluating it on multiple factors.This is the first step of selecting a mutual funds based on its rating, these rating are given by top rated credit agencies.

Expense Ratio

It is amount charged by Asset management companies to manage your investment,always give special attention to expense ration because your return on mutual funds is somewhere based on that,Always buy mutual funds of less expense ratio because more the expense ratio means less your return and less expense ratio means more return available to you.

AMC

AMC or asset management companies are the companies that runs and o manages the fund.Examples are HDFC Mutual Fund, ICICI Prudential Mutual Fund. List of AMCs is here. Top AMCs have good and professional fund managers.

Holdings

Holdings are the content of portfolio where the fund manager have invested the money.The holding shows you the percentage of money invested by fund manager across different sectors and different companies .These are names of companies whose shares or bonds are bought by the scheme.

Lock-In-Period

This is the given period of time till which the investment cannot be withdrawn. for example ELSS have a lock-in-period of over 3 years. It is the Period during which an investor is restricted from selling a particular investment

AUM

AUM or asset under management is the total value of investment a mutual fund scheme holds.

Fund Manager

Fund Manager is the person who invest and manages your money,he/she decides in which sector the money should be invested by thoroughly researching and analysing companies.

Entry Load

It is the percentage of fee levied on the purchase of mutual funds scheme, it reduced the investor’s investment For instance, a mutual fund scheme with 3% entry–load would deduct entry–load from the amount invested into the scheme and invest the remaining amount

Entry Load is a percentage of fee levied on the purchase of a mutual fund scheme. The levying of entry load reduces the investors’ investment.

Exit load

An exit load refers to the fee that the Asset Management Companies (AMCs) charge investors at the time of exiting or redeeming their fund units. . Not all funds levy an exit charge

In case of open-ended funds, the investors have the choice to exit the scheme as and when they want.

Sometimes, investors fail to stay invested for the specified period for which they had agreed to invest in a fund. Hence, an exit load discourages investors from prematurely exiting the fund.

Hence, while choosing a plan, do consider the exit load too, along with its expense ratio. You need to note that the exit load is not part of the expense ratio.

These are some of common terms that you first need to understand before investing in mutual funds because it always says “Mutual funds are subject to market risk,read all schemes related documents carefully” and yes there are risk in mutual risk and there is only one way to foregone the risk out by getting more knowledge about personal finance,there are various source to knowing about personal finance like books,blogs,financial advisers but the main thing is making yourself aware of it and don’t invest money without proper knowledge,So i hope you enjoy some knowledgeable stuff above.Thank You

So,as in the last blog i have written about mutual funds,its types etc. Now,i am gonna tell you some of its advantages that will surely benefits you and i will also write about what is sip,its advantages,swp,how it works and its advantages.All these things will be helpful for your decision regarding investment in mutual funds and also it will make you understand more about the pros and cons of mutual funds.

Reduction of risk through diversification

We can reduce our risk by investing in different securities across different sectors,if your investments in one sector is down then your investments in other sector will compensate it and you can also invest in goverment bond which is a risk free investment option where your money is safe.

If you invest in goverment bond it will protects you from a precipitous drop in stocks.

Managed by professionals

The money you invests in mutual funds is managed by a professional who have a deep knowledge in investment domain and also having better availability to research materials about the market and companies

He also know some money making strategy because of his experience you can trust him that he can take better investment decision for you which will further reduces risk

liquidity

Another advantage is the liquidity,which you get if you invests in mutual funds unlike stocks where it will take 2-3 days to get funds into your bank account whereas it is easier to buy and exit mutual fund scheme.

Low cost

If you buy more units of mutual funds then then processing fee and other charges will be reduce because of economies of scale which implies that if you buy more units then the marginal cost of per unit will be reduced for example if you one banana it costs you more but if buy a dozen then it will cost you less.

BETTER RETURN

Well there are other investment option also but if compare MFs to other financial products like FDs,nps then you definitely get a better return option here while the risk is always there but the risk is manageable because if you want to earn some extra bucks then you must invest in mutual funds.

FLEXIBLE AND CONVENIENT

Mutual funds are one of the most flexible investment option for people because almost everyone can avail the benefits of it,due to the fact that anyone can start sip with the minimal amount of 500 rupees it is accessible to all so anyone according to their income level can invest in mutual funds

It is also easy to use or convenient for people to invest in mutual funds due to the advancement of technology there are many apps through which you invest directly in mf at anytime from anywhere

SYSTEMATIC INVESTMENT PLAN(SIP)

SIPs are being popular post demonatization period and also Amfi’s Mutual Fund Sahi Hai campaign also helped popularising the concept of SIP and mutual funds.There are 2 ways you can invest money in mutual funds either through lumpsum or through SIPs,

In lumpsum, you invest a fixed amount only once and then you get return over it annually where as in SIP you invest a fixed amount regularly which is generally monthly and quarterly.So lets finds what exactly a sip is

SIP is a plan in which you can invest a fixed amount at regular intervals, generally monthly and quarterly,you can start sip with as low as 500 rupees and there is no maximum limit unless specifies

Why choose SIP

Through sip you can invest a fixed amount at regular intervals which means you can create wealth with small amounts

It gives you better return as compared to other investments like FDs,

You can start sip with a small amount of 500 rupees

you don’t need to research and analyse much as your investment is managed by professional who can do this work for you yet you have to analyse before investing in particular MF.

you can enjoy the power of compounding. When you invest over a long period and earn returns on the returns earned by your investment, your money would start compounding. This helps you to build a large corpus that help you to achieve your long-term financial goals with regular small investments.

SYSTEMATIC WITHDRAWAL PLAN

It is an investment plan in which one can withdraw a fixed amount at regular intervals which is generally pre determined date of month,it can be monthly,quarterly,semi-annually or annually.This facility is given by mutual funds to redeem fixed units at regular intervals

Retirees are most often reliant on SWPs for retirement income generated from investments accumulated in retirement accounts like IRAs or 401(k) plans

When you choose to use swp you need to aware of that your overall mutual funds value will be affected too because the nav(net asset value) will affect your overall value and withdrawal units of mutual funds.

HOW IT WORKS

if an investor bought 10000 units of mutual funds at the nav 10 rupees and wants to receive 10,000 rupees monthly than after receiving10,000 for the first month the remaining units held at investor is 9,000(10,000-1,000) while the NAV is 10. Now suppose the NAV is increase to 20 then the overall units held by investor after receiving 10,000 rupees in a second row is 8,500(9,000-500) because your nav has increased your units sold has been decreased which is good for you but the situation can fall opposite if your nav will decrease or reduced.

There are two withdrawal options available in SWP – Fixed Periodic withdrawal and Appreciation withdrawal.

Fixed Periodic withdrawal

In a fixed periodic withdrawal, an investor chooses a fixed amount to receive after interval specific time. Mutual fund house will sell units and transfer the amount in the investor’s account.

Appreciation Withdrawal

In appreciation withdrawal, an investor chooses to withdraw only the return generated on his corpus. For example, if an investor has a corpus of Rs 10cr in a mutual fund and the fund has given a return of 1% in last one month then he will only get Rs 10lakh for that month. Therefore, an investor can create a perpetuity using appreciation withdrawal; however the cash flow will not be same as returns are not fixed.

WHY TO CHOOSE SWP

The first benefit of this plan is you get a regular income on monthly basis,if you are retired person then it would be suitable for you to manage your daily expenses

swp creates an additional way of regular income for you

It helps you to meet your financial needs like .If you have a recurring expenses like house emi or car emi or child’s fees then you can use this plan and the return generated on your income will be spent on your these expenses.

these withdrawals, which are also referred to as redemptions, are not subject to tax deduction at source(TDS).

Mutual funds industry has been booming from past some years as people are becoming more interested in investing their money in that because of easy accessibility to invest and high return,this sector has attracted thousands of investors towards it and due to much more awareness about mutual funds through commercials,advertisement this industry has been surge greatly.So,as many millennials are also interested in investing in mutual funds i have decided to start a series of blogs to cover almost everything important about it.

Before starting i would like to share some key facts about mutual funds :

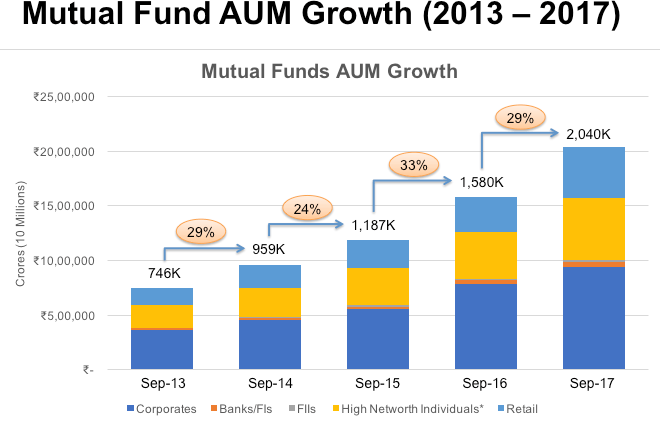

Assets Under Management(AUM) of Indian Mutual Funds Industry as on Feb 29,2020 stood at 28.94 lakh crore

AUM of Indian mutual industry grown from 7.6 trillion on feb 28,2010 to Feb 27.23 trillion as on Feb 27,2020 ,which is more than 3.5 times in merely 10 years

The industry had created the milestone of 10 lakh crore for first time in may 2014.

Total number of accounts as on Feb 2020 at 8.88 crore

what is mutual funds ?

Mutual funds are a pool of funds from various investors and is professionally managed by some experienced fund managers,who will further invest the accumulated amount into different sectors as per the financial goals of investors and other related factors.

There are different types of mutual funds scheme and as per the financial objective of investors,they should invest in mutual fund schemes. Mutual funds are become easy to invest option for investor as their is no more complexity related as compared to investing in share market,where one needs to proper analyse the stock fundamentally and technically and i agree that you still have to analyse before investing in mutual funds but there is more risk in losing money in share market as compared to mutual funds because of less volatility and also due to the fact that mutual fund are managed by more experienced and more knowledgeable manager, they can invest more properly than retail investors. The primary aim of a mutual fund scheme is to create wealth or earn income by investing in diverse assets.

Types of Funds

Open-Ended funds

Open-ended means one can enter and exit the fund anytime, at daily NAV(it is the value of per unit of mutual funds. For example, you can exit from equity funds, which are essentially long-term products, within 6 months.

For example : ICICI Prudential Banking and Financial Services Fund, Motilal oswal multicap 35 funds

Close-Ended funds

These funds are majorly used for long-term investments mainly for 3 to 5 years to avoid the volatility caused by huge redemption

It means one can exit after a certain period on expiry of the term, the portfolio is liquidated and the funds are distributed

Close end funds also has liquidity option these funds are listed on the exchange where one can sell their units to another at listed price,and list price is mainly lower than NAV

Interval funds

Investor funds are suitable for those who wants to invest for long term but also wants the liquidity feature

Interval funds are a type of close end funds that become open to transaction during a preset interval periods,for example first 5 days

Fees for interval funds tend to be higher than for other types of mutual funds, as do returns

To get the liquidity feature in close-ended funds, there is another category called ‘interval’ funds. Essentially, these are close-ended funds that become open to transactions during preset interval periods, for instance, first 5 days of every quarter.

Active vs passive funds

Active funds are those funds in which the funds manager actively buy and sell securities based on his knowledge,expertise on market,sector and economy.

Because of the fact that fund manager actively buy and sell security,the expense ratio is also higher than passive managed funds.

It also sees that sometime fund manager can able to outperform the market and generate higher return.

Passive funds are those funds which imitate the market indices such as S&P BSE sensex or NIFTY 50 means the return on your money invested in mutual funds is based on the market index if the index rises then your return also rise or vice-versa.

As passively managed funds doesn’t demand research and analysis,the expense ratio is also seemed to be lower than active funds

You can track the performance of your mutual funds by just analysing the performance of the market index,for example if the market indices rise to 2% than your money did the same thing.

Debt,equity and hybrid funds

Debt funds

A debt funds is a fund that invest in fixed income securities like bonds,commercial papers,debentures etc.

On average, the fee ratios on debt funds are lower than those attached to equity because the overall management costs are lower.

Debt funds are characterised by length of time period such as Money market funds or instrument are for shorter term mainly for 6-12 months and long term which has horizon for more than 1 year

Debt-funds are less riskier than equity funds

Types of debt funds

Liquid/money market funds

The money is invested in money market instrument like treasury bills etc which have a maturity period of 91 days,this funds offers lower return as compared to other long term horizon funds

Income Funds

Income funds invest in a mix of government and corporate fixed income securities such as bonds, debentures and commercial papers with extended maturity period.These funds have a stability than other funds.. The average maturity of income funds is around 5-6 years.

Ultra Short Term/Short Term Funds :

Those investors who wants to invest for 6 months to 1 year can invest in ultra short term or short term funds because of the high maturity period the returns over this funds is also high.

Gilt funds

Gilts funds invest only in high rated government securities like treasury bills and government bonds. These funds are considered to have no credit risk since government securities are considered to be risk free.These funds offers lower risk as compared to others but it is suitable for those investors who wants their money to be safe.

Fixed Maturity Plans (FMPs)

Fixed maturity plan are a part of close end funds.They have a fixed maturity period ranging from 3 months to 5 years,these funds also invests in fixed income securities like corporate bonds and the government securities one should invest in this funds to keep their money safe but don’t expect a higher return.

Equity funds

An equity mutual funds is primarily invested in stocks.It can be actively or passively (index fund) managed.Equity mutual funds are more riskier than debt funds because of higher volatility in equity funds but equity funds have the potential to give you far better return than debt funds.

Types of Equity funds :

Large-cap equity funds :

These funds includes stocks of top 100 major companies as per market capitalisation(current price of stock 8 X no of shares issued) across all sectors,these funds are also called (BIG-CAP) and the market capitalisation of large cap funds is above 10,000 crore rupees

Because of their market capitalisation is so large,investor have to tend to believe on safety of invested money and further growth of company

These funds are typically used as core long-term investments in an investment portfolio because of their stability and dividends

Mid-Cap Equity Funds

These funds includes stocks of emerging companies whose market capitalisation is lower than large cap funds but have a potential to grow and give higher return.The market capitalisation of mid-cap funds is between 2,000 to 10,000 crore rupees

Mid-cap stocks are useful in portfolio diversification as they provide a balance of growth and stability but they are more riskier than large cap funds

Small/Micro Cap Equity Funds

These funds invested in small companies having market capitalisation of below 2,000 crore rupees

These funds have potential to give higher return than the large and mid-cap companies but one need to choose it wisely because these funds are more riskier than large and mid cap companies you can even lose own money in these funds

These firms have experience higher volatility, even some of the small cap company can go bankrupt also.These funds are suitable for those who can bear more risk in return of higher potential.

Equity Linked Savings Schemes (ELSS)

These are the widely known funds for tax saving,many people invests in this fund to save the tax paid by him These funds offer tax benefits upto Rs 1.50 lakh under Section 80 C of Income Tax Act.

Hybrid Funds

Hybrid funds are the combination of equity and debt funds and due to that these funds have potential to offers higher returns than a regular debt fund while not being as risky as equity funds.

One should invest in hybrid funds to achieve diversification and avoid the concentration risk.

Types of Hybrid funds

Monthly Income Plan (MIPs)

MIPs invest a large potion in AUM in debt securities for safety of investment and small portion in equity funds for higher returns.

Balanced Funds

Balanced funds are those funds which invest a significant portion in either debt securities or equity market. If a balanced fund has allocated more than 65% of its AUM to equity and equity related instruments, and rest in fixed income securities, it is called ‘Equity-oriented Balanced Fund’.

On the other hand if its investment in equities is less than 65% then it is called ‘Debt-oriented Balanced Fund’.

Well,mutual funds is better option for investment for people who doesn’t have good knowledge about stock market and also for investor who doesn’t want to take more risk as stock investing because investing in stock is very riskier as well as demand more capital.So,mutual funds are best suitable for millennial who just starts earning and wants to invest money anyone can start investing in mutual funds with as low as 500 rupees and it will creates value for you in future. So this is the first blog in the series about mutual funds we will back to you with further more.